Category: Retirement Planning Audience: Beginner, young investors, diaspora investors, self-employed workers Reading time: 6 minutes Slug: /education/dollar-cost-averaging-continuous-investing

Summary

Dollar-cost averaging means investing a fixed amount on a regular schedule, instead of waiting for the “perfect” time. For many Cameroonian investors, it can turn monthly income, business profits, or diaspora remittances into a long-term retirement habit.

Article

Dollar-cost averaging, often called DCA, is a simple investment habit: you invest the same amount regularly, regardless of whether the market is up or down.

For example, instead of trying to guess the best day to buy a broad market ETF, an investor might invest 25,000 FCFA every month. When prices are high, that amount buys fewer shares. When prices are low, it buys more shares. Over time, the investor builds ownership gradually without trying to predict the market.

This matters because many people do not receive one large amount to invest. A salary earner, trader, freelancer, doctor, engineer, teacher, civil servant, business owner, or diaspora worker may build wealth from monthly cash flow. DCA converts that cash flow into discipline.

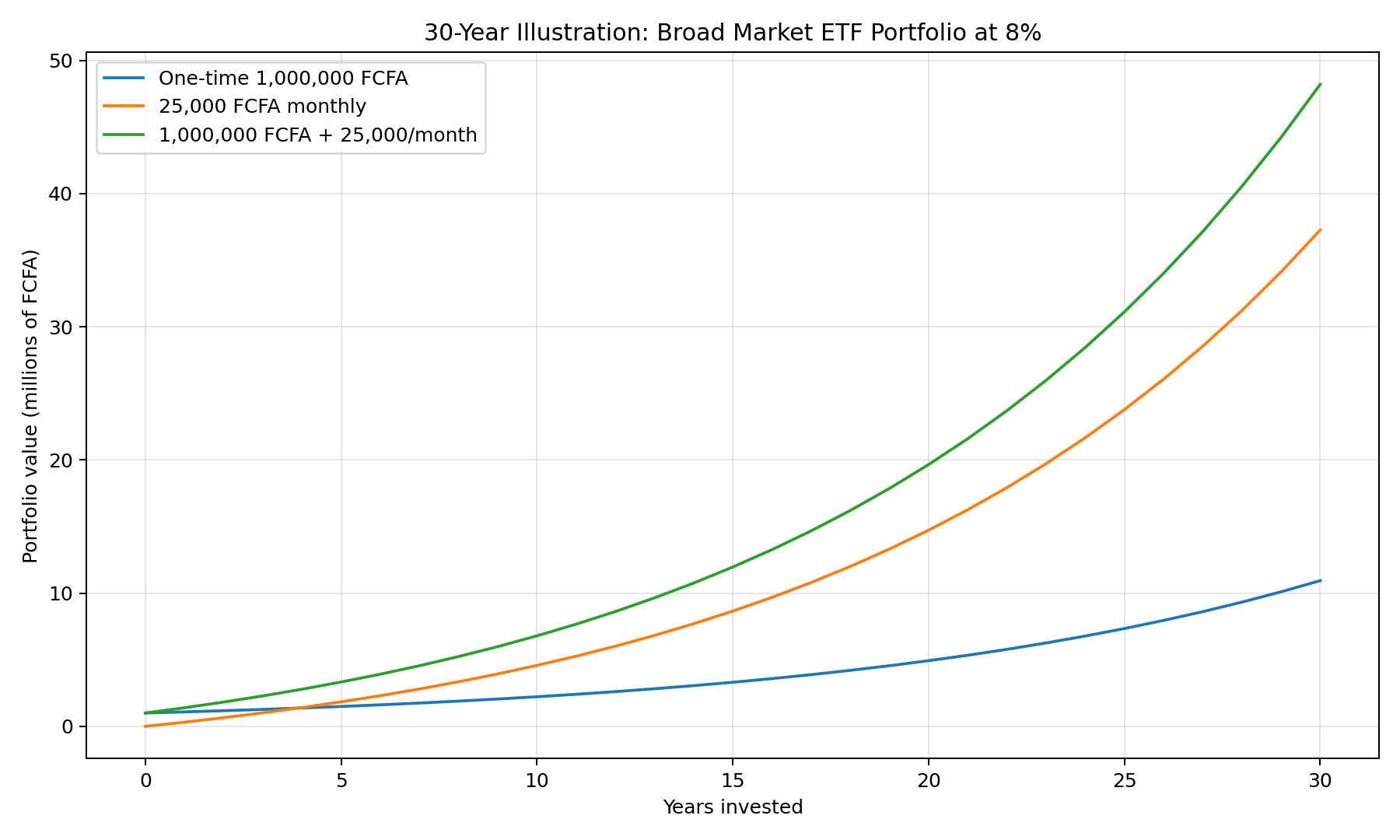

Practical 30-year example: broad market ETF portfolio

Assume an investor uses a diversified broad market ETF-style portfolio and earns an educational average return of 8% per year. This is not a promise. Real markets can lose money, sometimes for long periods.

| Scenario | Initial amount | Monthly investment | Total contributed | Approximate value after 30 years |

|---|---|---|---|---|

| One-time contribution only | 1,000,000 FCFA | 0 FCFA | 1,000,000 FCFA | 10.94M FCFA |

| Continuous investing | 0 FCFA | 25,000 FCFA | 9,000,000 FCFA | 37.26M FCFA |

| Start + continue | 1,000,000 FCFA | 25,000 FCFA | 10,000,000 FCFA | 48.19M FCFA |

| Same-total lump-sum benchmark | 9,000,000 FCFA | 0 FCFA | 9,000,000 FCFA | 98.42M FCFA |

The lesson is not that monthly investing always beats lump-sum investing. The lesson is that continuous investing creates a habit. The person who invests every month keeps adding fuel to the engine.

A fair comparison is important. If someone already had the full 9,000,000 FCFA available on day one and invested it for 30 years, that lump sum could grow more than monthly contributions because the full amount has more time in the market. But most people do not have 9,000,000 FCFA waiting. They build from income.

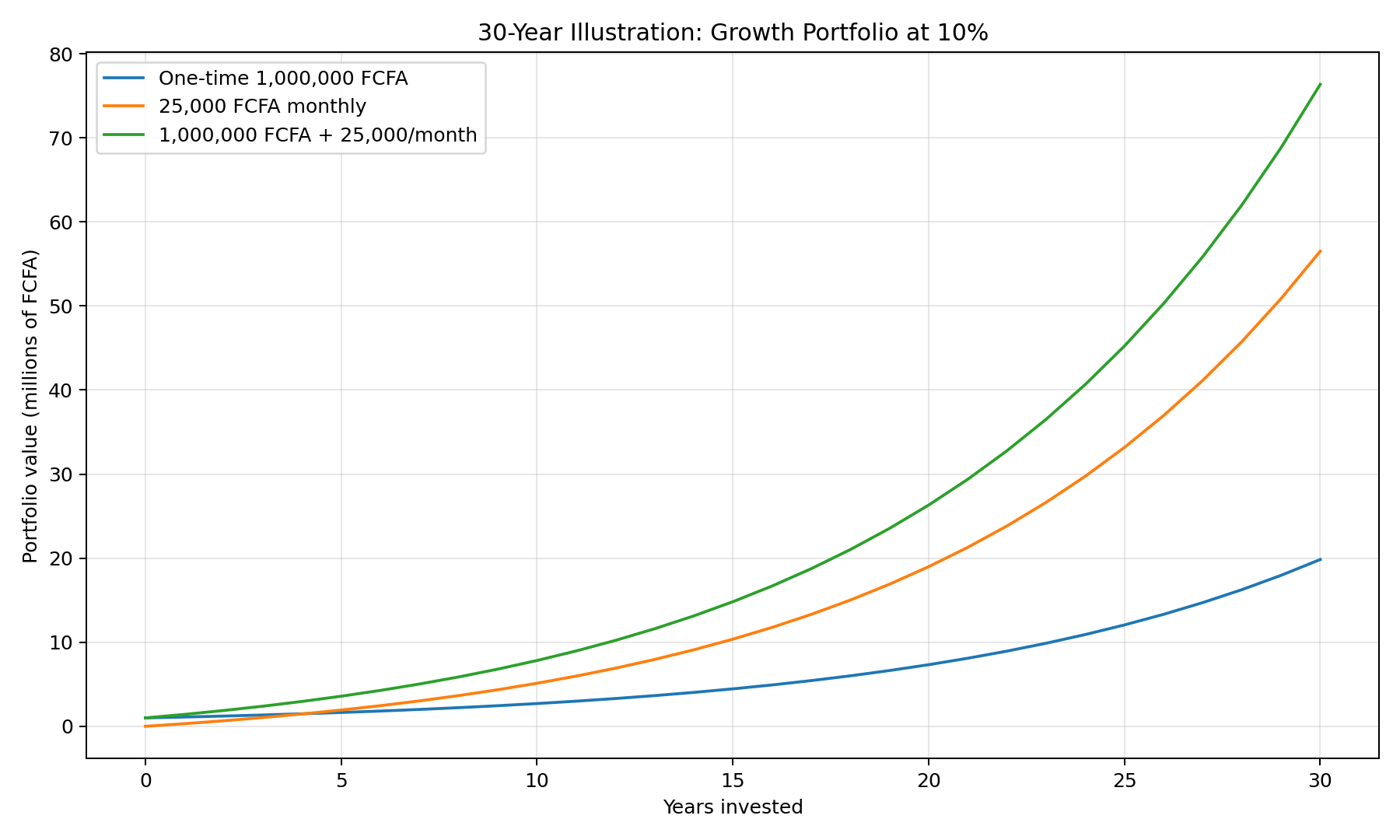

Practical 30-year example: growth portfolio

A growth-oriented portfolio may target higher long-term returns but usually comes with higher volatility. Assume an educational 10% annual return.

| Scenario | Initial amount | Monthly investment | Total contributed | Approximate value after 30 years |

|---|---|---|---|---|

| One-time contribution only | 1,000,000 FCFA | 0 FCFA | 1,000,000 FCFA | 19.84M FCFA |

| Continuous investing | 0 FCFA | 25,000 FCFA | 9,000,000 FCFA | 56.51M FCFA |

| Start + continue | 1,000,000 FCFA | 25,000 FCFA | 10,000,000 FCFA | 76.35M FCFA |

| Same-total lump-sum benchmark | 9,000,000 FCFA | 0 FCFA | 9,000,000 FCFA | 178.54M FCFA |

Why DCA is useful for retirement planning

Dollar-cost averaging can help investors avoid three common mistakes.

First, it reduces the pressure to time the market. No one knows the perfect day to invest. A regular schedule removes some emotion from the decision.

Second, it builds consistency. Retirement planning is not usually built from one dramatic decision. It is built from hundreds of small decisions repeated over many years.

Third, it works well with real life. A self-employed person can invest a percentage of monthly profit. A diaspora investor can invest part of each paycheck. A young professional can start small and increase contributions as income grows.

What DCA does not do

DCA does not guarantee profit. It does not protect against bad investments. It does not remove currency risk, tax issues, platform risk, or market risk.

It also may underperform a lump-sum investment when markets rise over the investing period. This is why DCA should be explained honestly. It is not magic. It is a disciplined method for people who invest from recurring income or who want to reduce emotional timing risk.

How Cameroonian investors can think about it

For a Cameroonian investor, DCA can be adapted to income patterns:

- Monthly salary contribution

- Weekly business-profit contribution

- Quarterly professional bonus

- Diaspora remittance allocation

- Annual business surplus split into monthly entries

The key is to choose an amount that is realistic. It is better to invest 10,000 FCFA consistently than to plan for 100,000 FCFA and stop after two months.

Key takeaway

Continuous investing is powerful because it combines discipline, time, and compounding. For retirement planning, the most important question is not “Can I predict the market?” It is “Can I build a habit that I can continue for decades?”

Educational note

This article is for general education only. It is not investment, legal, tax, brokerage, foreign-exchange, or retirement advice. InvestCam is currently an education, waitlist, and sandbox demo platform only. No live deposits, withdrawals, FX conversion, securities trading, or investment execution are currently enabled.