Category: Cameroon & Global Investing Audience: Beginner, diaspora investors, entrepreneurs, self-employed workers Reading time: 6 minutes Slug: /education/njangi-vs-stocks-saving-investing-growth

Summary

Njangi is a powerful community savings system in Cameroon. Stocks and ETFs are different: they are ownership investments designed for growth, but they carry risk. Understanding the difference helps families use each tool for the right purpose.

Article

Njangi is one of Cameroon’s most familiar financial systems. A group of trusted people contributes a fixed amount weekly or monthly. Each cycle, the collected money is given to one member. The rotation continues until every member has received the pot.

Njangi is not ignorance. It is financial organization. It builds discipline, trust, social connection, and access to lump sums. Many businesses, school fees, emergencies, weddings, market stalls, and family projects have been funded through Njangi.

But Njangi and stock-market investing do different jobs.

How Njangi works

Imagine 10 members contribute 50,000 FCFA each month. The monthly pot is 500,000 FCFA. In month one, one member receives 500,000 FCFA. In month two, another member receives 500,000 FCFA. The cycle continues until every person has received one payout.

If everyone completes the cycle, each person contributes 500,000 FCFA and receives 500,000 FCFA. There is usually no interest. The value is not investment return. The value is forced saving, discipline, community trust, and access to a lump sum.

That is very useful for short-term goals.

How stocks and ETFs work

A stock represents ownership in a company. An ETF usually represents a basket of investments, such as many companies in one fund.

When you invest in stocks or ETFs, you are not waiting for your turn to receive a pot. You are buying ownership that can rise or fall in value. The goal is long-term growth, income, or both.

This can help with retirement planning because invested money may compound over decades. But unlike Njangi, the value is not fixed. It can go down. The investor can lose money.

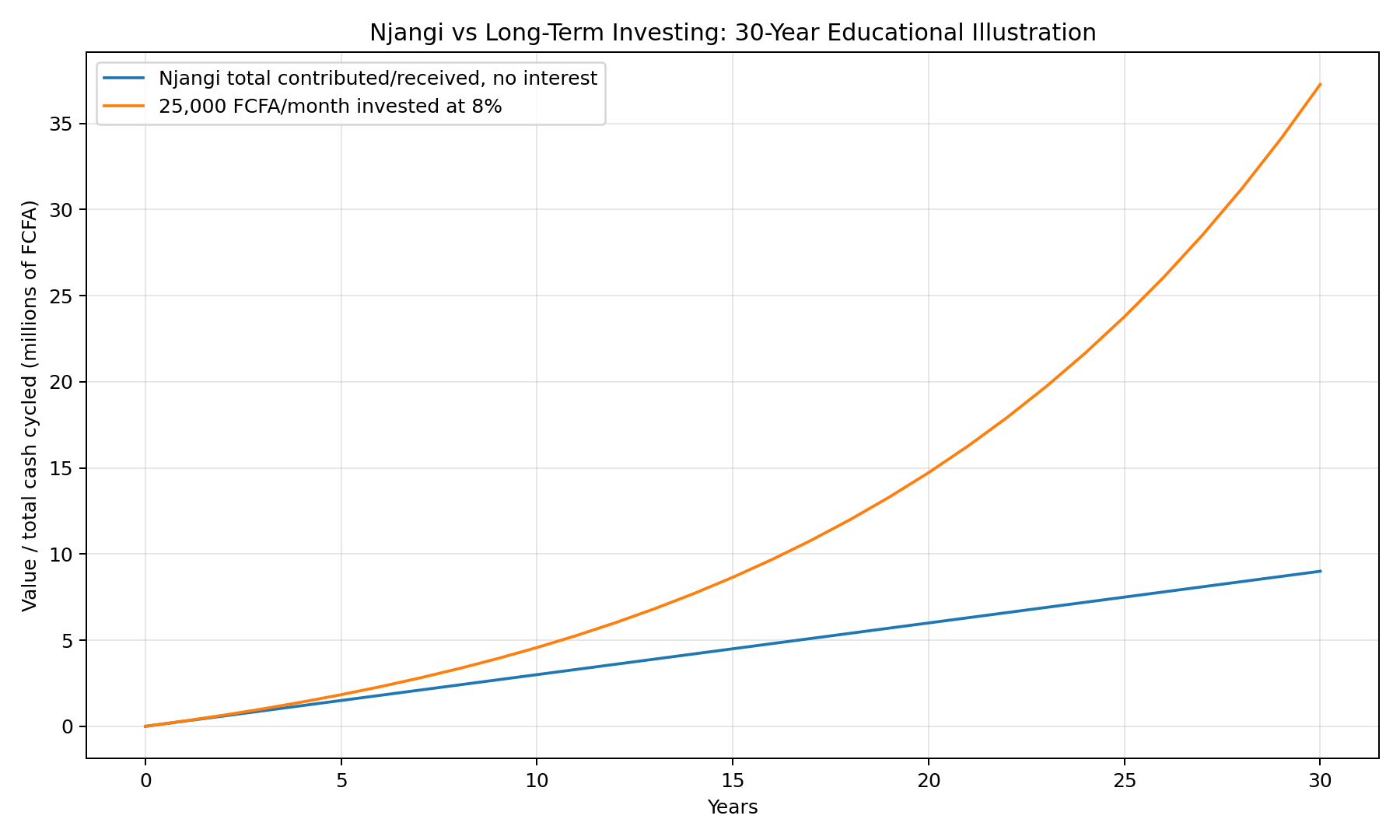

30-year illustration: Njangi cash cycle vs investing habit

Assume someone sets aside 25,000 FCFA per month for 30 years.

If that money only moves through repeated Njangi cycles with no interest, the total amount contributed and received over time is 9,000,000 FCFA. Njangi may still be useful because it provides lump sums at different points, but it does not create investment growth by itself.

If the same 25,000 FCFA per month is invested in a diversified broad market portfolio at an educational 8% annual return assumption, it could grow to about 37.26M FCFA after 30 years.

This example is not a promise. Stocks and ETFs can lose value. But it shows the difference between saving without interest and investing for long-term growth.

Njangi is good for some goals

Njangi can be excellent for:

- Short-term savings discipline

- School fees

- Business inventory

- Wedding or family obligations

- Emergency lump sums

- Community support

- People who need social accountability

It can also be useful when formal credit is unavailable, expensive, or slow.

Stocks and ETFs are better suited for other goals

Stocks and ETFs may be better suited for:

- Long-term retirement planning

- Wealth building over 10, 20, or 30 years

- Diversification outside one local economy

- Participating in the growth of large companies

- Building assets that can compound over time

But they require education, patience, risk control, and proper regulation.

The hidden issue: inflation

If a Njangi contribution has no interest, the amount you receive later may buy less than the same amount today. Inflation reduces purchasing power over time.

For example, receiving 500,000 FCFA today is not the same as receiving 500,000 FCFA many years from now if prices have increased. This does not make Njangi bad. It simply means Njangi is mainly a savings and cash-flow tool, not a full retirement growth strategy.

The right question is not “Njangi or stocks?”

The better question is: what is the job of each tool?

A family can use Njangi for short-term discipline and community support while also using regulated investment products for long-term retirement planning. A diaspora investor can support family Njangi commitments while also building a separate long-term portfolio. A business owner can use Njangi for working capital and invest a different portion of profits for retirement.

The danger is using one tool for the wrong job.

Do not put money needed for next month’s Njangi obligation into stocks. Markets can fall at the wrong time. Also, do not assume Njangi alone will create retirement wealth if it produces no investment return.

Key takeaway

Njangi is a respected community savings system. Stocks and ETFs are ownership investments. Njangi can help people save and access lump sums. Stocks and ETFs can help build long-term wealth, but with risk. A strong financial plan can respect both traditions while using each one correctly.

Educational note

This article is for general education only. It is not investment, legal, tax, brokerage, foreign-exchange, or retirement advice. InvestCam is currently an education, waitlist, and sandbox demo platform only. No live deposits, withdrawals, FX conversion, securities trading, or investment execution are currently enabled.